31 October 2023

Market News

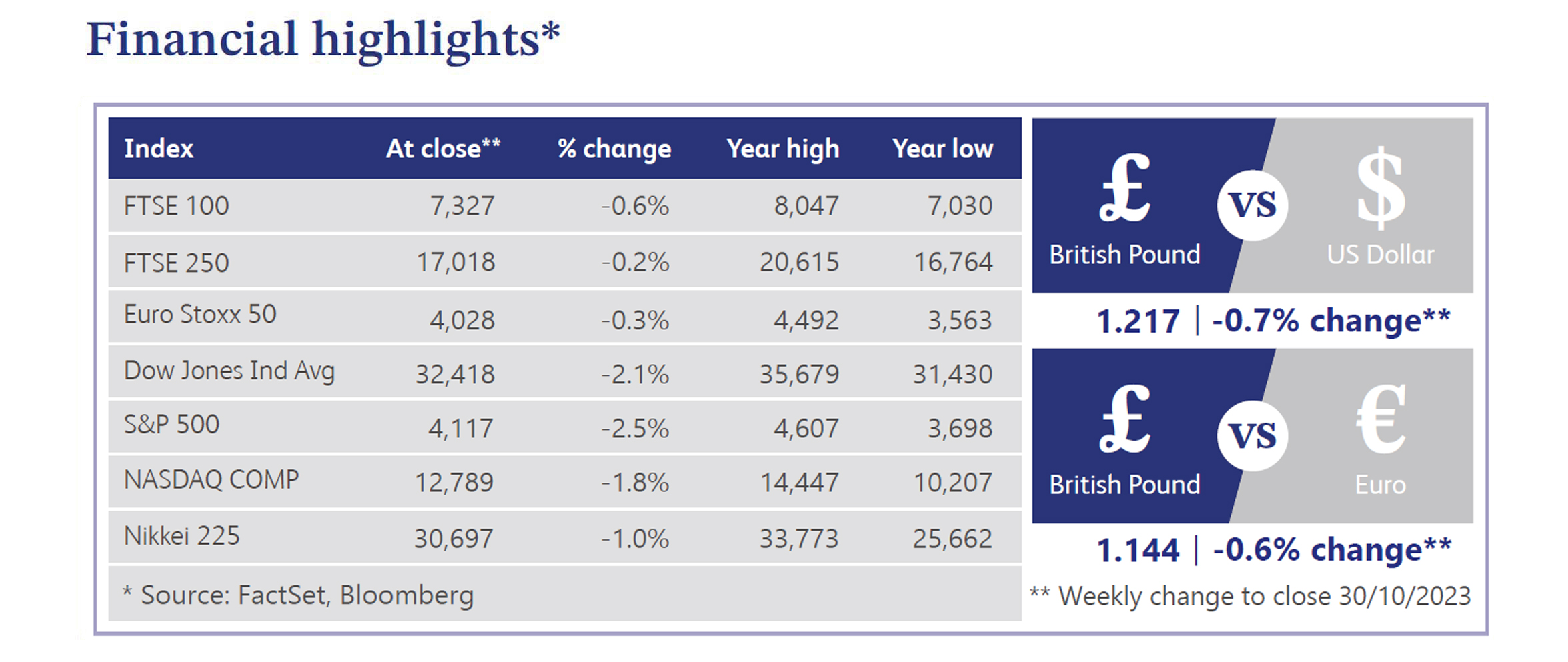

The UK's economic landscape experienced several developments last week. Borrowing costs surged to their highest point in 25 years as the 30-year UK gilt yield reached 5.209%. This increase mirrored global trends as investors worldwide anticipate interest rates will remain at elevated levels for a longer period than first expected. Despite this, a Reuters survey of economists indicated that the Bank of England's rate cycle might have peaked, with expectations of rates remaining on hold until the second quarter of 2024. Inflation risks were acknowledged, though the labour market seemed to stabilise. The majority foresaw the first rate cut, if needed, occurring no earlier than July, with a 0.25% reduction. In parallel, the UK labour market displayed challenges, with the benefit claimant count showing a substantial rise by 20,400, exceeding consensus estimates of a 2,300 increase. Notably, uncertainty around the Labour Force Survey prompted the introduction of a new data series for the unemployment rate by the Office for National Statistics, revealing a 4.2% unemployment rate, up by 0.2% from the previous quarter. Payrolled employment saw a decline and average weekly earnings eased.

A survey by BDO showed that medium-sized UK firms expressed apprehensions regarding rising material costs and supply chain disruptions potentially impacting their revenue during the crucial "golden quarter." Supply chain breakdowns and higher energy costs could lead businesses to transfer these expenses to consumers, potentially dampening demand. Additionally, concerns about the cost of living might result in reduced consumer spending during the holiday season, affecting businesses' revenues. Furthermore, higher oil and gas prices, along with logistical disruptions stemming from the Israel-Hamas conflict, compound these issues. Meanwhile, research by Allica Bank showed that small and medium-sized businesses in the UK find themselves disadvantaged compared to larger enterprises in terms of savings rates, potentially missing out on approximately £7.5 billion annually.

In the energy sector, the Telegraph reported that the Chief Executive Officer of National Gas underscored the continued reliance on fossil fuels in the UK to avert blackouts, particularly given the increased use of intermittent renewable energy sources. It has been suggested that gas is expected to play a crucial role in the energy landscape until at least 2040. In addition, Tom Glover, the Chair of RWE's UK arm, a multinational energy company, called for increased pricing, by as much as 70%, for wind farm operators to stimulate further construction off Britain's shores. In the housing market, Lloyds Bank predicted a continued decline in house prices until 2025, primarily due to expectations of sustained higher interest rates. This was a similar story as Bloomberg reported that UK landlords are selling properties at triple the pace compared to two years ago, mainly due to higher rates and increased regulations. Around 15% of rental property owners are expected to exit the market this year, potentially impacting house prices and rental rates.

Natwest Group, one of Britain's leading high street banks, saw its share price tumble approximately 17.8% last week after announcing its third quarter results. The results showed that total income was behind expectations at £3.49 billion for the period, compared to forecasts of £3.59 billion. One of the key negative catalysts was a weak outlook, leading to a lowering of its net interest margin guidance for the year. Natwest also discussed the closure of the accounts for Nigel Farage, where an independent review found that the decision was lawful, but that ‘serious failings’ were present.

Barclays, the UK based global financial services provider, announced its third quarter results last week. The company announced revenue of £6.26 billion, slightly falling short of expectations of £6.29 billion. Barclays did, however, announce that it is evaluating actions to reduce structural costs to help drive future returns, which may result in material additional charges in the final quarter of 2023. The bank also announced a weaker outlook and a lowering of its net interest margin guidance for 2023. The shares closed the week down approximately 10.8%.

Third quarter results for International Consolidated Airlines Group (also released last week), saw its shares end the week approximately 2.9% higher. The company announced a strong set of results with revenue of €8.65 billion compared to €7.33 billion a year ago, as well as profit after tax of €1.23 billion compared to last year’s figures of €853 million. Despite strong results, the company also mentioned a cautious outlook due to the wider macroeconomic and geopolitical uncertainties.

Market Commentary prepared by Walker Crips Investment Management Limited.

This publication is intended to be Walker Crips Investment Management’s own commentary on markets. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice you should contact your financial adviser or your usual contact at Walker Crips. Walker Crips Investment Management Limited is authorised and regulated by the Financial Conduct Authority and is a member of the London Stock Exchange. Registered office: Old Change House, 128 Queen Victoria Street, London, EC4V 4BJ. Registered in England and Wales number 4774117.

Important Note

No news or research content is a recommendation to deal. It is important to remember that the value of investments and the income from them can go down as well as up, so you could get back less than you invest. If you have any doubts about the suitability of any investment for your circumstances, you should contact your financial advisor.

The value of investments can fall as well as rise. Investors may get back less than invested. Past performance is not a reliable indicator of future results.

The value of investments can fall as well as rise. Investors may get back less than invested.