1 July 2025

The UK economy presented a mixed picture last week. Retail sales fell for the ninth consecutive month, with the Confederation of British Industry (“CBI”) survey revealing a sharper decline in June and pointing to further weakness in July. Although the composite Purchasing Managers' Index (“PMI”) rose slightly to 50.7, signalling marginal growth, manufacturing output remained subdued, and consumer sentiment held flat, reflecting ongoing economic uncertainty. Long-term inflation expectations ticked higher, raising concerns over future price stability, while food inflation accelerated to 4.7%, underscoring persistent cost pressures. The Bank of England (“BoE”) maintained a cautious stance: Governor Andrew Bailey defended quantitative easing, while Monetary Policy Committee members Megan Greene and Dave Ramsden expressed diverging views on the direction of interest rates. Adding to the subdued outlook, the Resolution Foundation projected stagnant household incomes until 2030, highlighting sustained challenges to living standards. Overall, despite signs of resilience in certain areas, underlying pressures continue to weigh on the UK’s growth outlook.

The UK’s fiscal outlook grew increasingly complex last week amid rising policy tensions. Chancellor Rachel Reeves’ proposed £5 billion welfare cuts encountered strong internal opposition, with over 100 Labour MPs backing an amendment to block the reforms — prompting discussions to dilute the bill. The Institute for Fiscal Studies (“IFS”) cautioned that even with the proposed changes, welfare spending is projected to rise by £8 billion by the end of the decade. At the same time, the government launched a 10-year industrial strategy, which included green levy reductions for over 7,000 firms, though the estimated annual savings remain modest at around £15 million. Business groups such as the British Chambers of Commerce (“BCC”) urged a tax freeze, citing job losses tied to higher national insurance contributions. Meanwhile, a rise in Chinese exports to the UK — partly driven by US tariffs — added to inflationary concerns. Fiscal pressures were further compounded by record millionaire outflows following changes to non-dom tax rules. The Resolution Foundation warned that Reeves may ultimately require tax increases to fund potential welfare U-turns and mounting benefit costs.

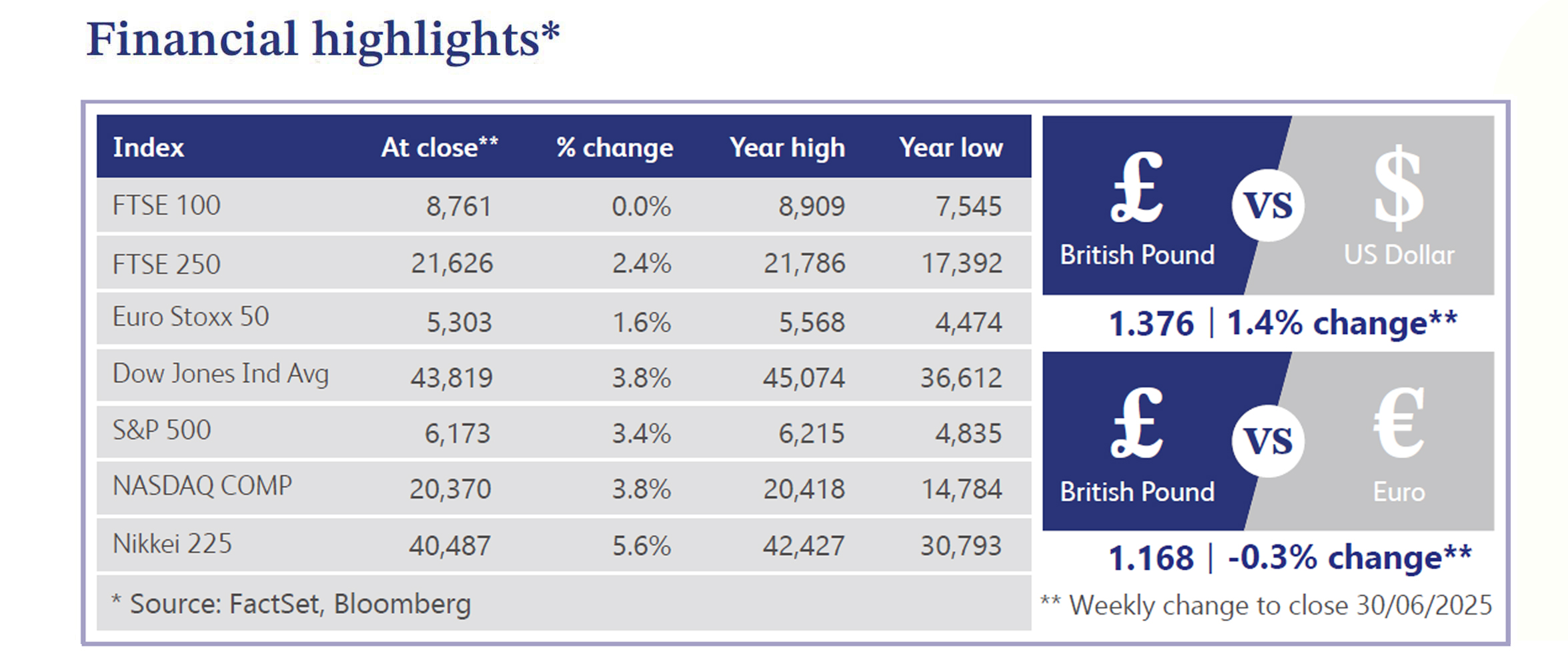

UK equity markets remained resilient last week, buoyed by robust merger and acquisition (“M&A”) activity and sterling strength. M&A volumes surged 52% year-on-year in H1 2025, with 1,207 deals totalling $118.6 billion — marking the busiest quarter since Q2 2022. Improved political stability and declining interest rates have revived investor confidence, particularly among private equity firms and international buyers. Sterling recorded its strongest weekly gain in four months, supported by broad dollar weakness and rising foreign inflows. Meanwhile, Bloomberg reported that the City of London is actively courting Chinese firms to revive initial public offering (“IPO”) activity, reinforcing efforts to revitalise London’s capital markets amid a slowdown in listings.

US equities rallied, with the S&P 500 and Nasdaq reaching fresh record highs. Sentiment was lifted by easing geopolitical risks following a de-escalation in Israel-Iran tensions, as well as positive trade signals. Big tech led the advance, with Nvidia (+9.7%) and Meta (+7.5%) outperforming. Rate-sensitive sectors, including banks, autos and semiconductors, also gained. US Treasury yields fell sharply, with the 2-year dropping to 3.75%, while the dollar index declined 1.5%. WTI crude slumped 11.3% as Middle East supply concerns abated. Markets have increasingly priced in looser Federal Reserve policy, especially amid speculation that Donald Trump may replace Jerome Powell early, with 0.64% of rate cuts now expected by year-end.

JD Sports Fashion rallied 20.5% after Nike’s earnings proved less weak than feared. Nike’s renewed support for wholesale partners was seen as a positive for JD, a key retail collaborator. However, Citi cautioned that Nike’s inventory clearance could weigh on JD’s near-term margins. Nike also highlighted rising tariff costs and efforts to reduce reliance on Chinese manufacturing for the US market. This may benefit JD’s supply chain and wholesale exposure in the longer term, especially if trade routes shift. Investor optimism focused on JD’s potential to capitalise on structural shifts in global retail sourcing and wholesale alignment with top brands.

Babcock International rose 7.9% after delivering strong Full Year 2025 results, supported by higher global defence and energy security spending. Organic revenue climbed 11% to £4.83 billion, led by marine (+12%) and nuclear (+19%). Underlying profit rose 17% to £247.1 million. The company announced a £200 million buyback and 30% dividend increase, alongside upgraded margin guidance of 9% or more by Full Year 2027. Management now expects to hit its 8% margin target a year early in Full Year 2026. Berenberg raised its target price and Full Year 26–28 earnings per share (“EPS”) forecasts, citing long-term growth drivers as defence budgets rise globally. Market confidence remains strong amid sector tailwinds.

Rolls-Royce Holdings climbed 7.5% after a US-UK trade deal scrapped the 10% tariff on aircraft engines and parts, boosting investor sentiment. The move is expected to enhance cost competitiveness for Rolls-Royce in transatlantic markets, especially benefiting its Civil Aerospace division. The Aerospace and Defence index also gained, with the tariff removal viewed as a catalyst for sector-wide growth. Analysts anticipate improved export prospects and margin support. Defence investment trends further strengthen Rolls-Royce’s outlook, adding to momentum from civil and military demand. The company was among the FTSE 100’s top performers, reflecting optimism over trade-driven expansion and earnings upside.

Market Commentary prepared by Walker Crips Investment Management Limited.

This publication is intended to be Walker Crips Investment Management's own commentary on markets. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice you should contact your financial adviser or your usual contact at Walker Crips. Walker Crips Investment Management Limited is authorised and regulated by the Financial Conduct Authority (FRN:226344) and is a member of the London Stock Exchange. Registered office: 128 Queen Victoria Street, London, EC4V 4BJ. Registered in England and Wales number 4774117.

Important Note

No news or research content is a recommendation to deal. It is important to remember that the value of investments and the income from them can go down as well as up, so you could get back less than you invest. If you have any doubts about the suitability of any investment for your circumstances, you should contact your financial advisor.

The value of investments can fall as well as rise. Investors may get back less than invested. Past performance is not a reliable indicator of future results.

The value of investments can fall as well as rise. Investors may get back less than invested.