2 June 2026

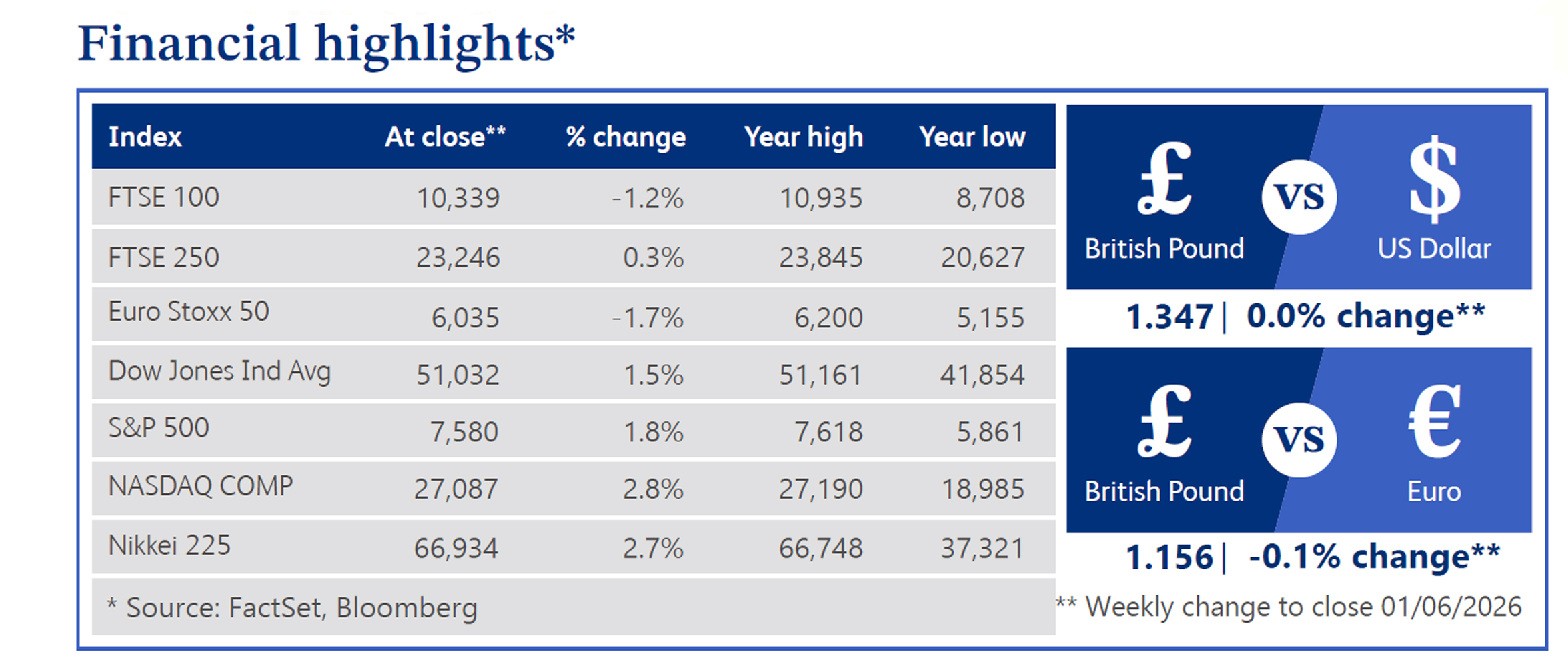

Last week, Britain's economic landscape continued to struggle due to the energy shock driven by the conflict in Iran, leading to Ofgem (“the Office of Gas and Electricity Markets”) announcing a 13% rise in energy bills. This and other inflationary measures mean the headline inflation will likely remain above the BoE’s (“Bank of England”) target for a fifth consecutive year. BoE Governor Andrew Bailey indicated that while rate cuts are off the table, recent bond market tightening has bought the central bank time to monitor the conflict's volatility. Investors have subsequently scaled back their interest rate expectations, pricing in just a small increase by year-end. There is also stagnation in the labour market. Resignation rates have dropped to 0.55%, with workers clinging to existing roles due to fewer vacancies; higher employer taxes; and automation threats.

In Downing Street, Labour is facing criticism from former Prime Minister Tony Blair, who publicly warned Prime Minister Keir Starmer of having no concrete plan and shifting the Labour government too far to the left. Starmer hit back, claiming Blair’s views are outdated, with broader members of Labour seemingly agreeing with Starmer. Despite this, Starmer’s premiership remains contested by internal hopefuls. Fiscally, this uncertainty is increasing Britain's borrowing costs, as lingering pandemic bills push public debt toward 94% of GDP ("Gross Domestic Product"). Chancellor Rachel Reeves has ordered ministers to prioritise domestic contracts in sectors like steel and artificial intelligence (“AI”). Meanwhile, a post-Brexit trade reset is underway, with officials confirming a deal to eliminate costly European veterinary certificates and border bureaucracy, by mid-2027 to help support exporters.

In the markets, gilt yields remain elevated as institutional investors demand a higher risk premium for UK debt, leaving British 10-year yields the highest amongst advanced economies. Investment banks note that these pressures have left UK equities looking cheap compared to global peers, although sentiment is divided. While private equity interest in professional services is cooling due to technology disruption risks, major high-street retailers are aggressively lobbying for new import tariffs to counter Chinese rivals. Meanwhile, representatives for major banks are pushing the Treasury to expand the state growth guarantee scheme to £5 billion to increase small-business lending, betting on a tech-driven and services-led productivity recovery over the longer term.

Across the pond, US equity indices climbed to record highs, as the S&P 500 rose 1.8% led by a rally in the technology and semiconductor sectors, while energy and consumer staples lagged behind. In commodities, gold advanced, whereas oil prices fell. This drop in crude, combined with a decline in Treasury yields, came as investors priced in optimism over a potential 60-day ceasefire agreement with Iran, which now awaits final approval from President Donald Trump. Economic data showed that sentiment remained resilient as the market balanced sticky inflation data at 3.3% year-on-year, against a lower probability of interest rate hikes. The broader market narrative was supported by the AI rally, following strong earnings from both software and hardware technology.

The UK housing market slowed in May, as the Nationwide house price index fell month-on-month. This was the first monthly decline this year, and price growth also slowed on an annual basis. Higher mortgage rates and energy shocks have heavily weighed on consumer confidence. Even though property listings hit an 11-year-high, weak demand has frozen the market, particularly at the more expensive top end.

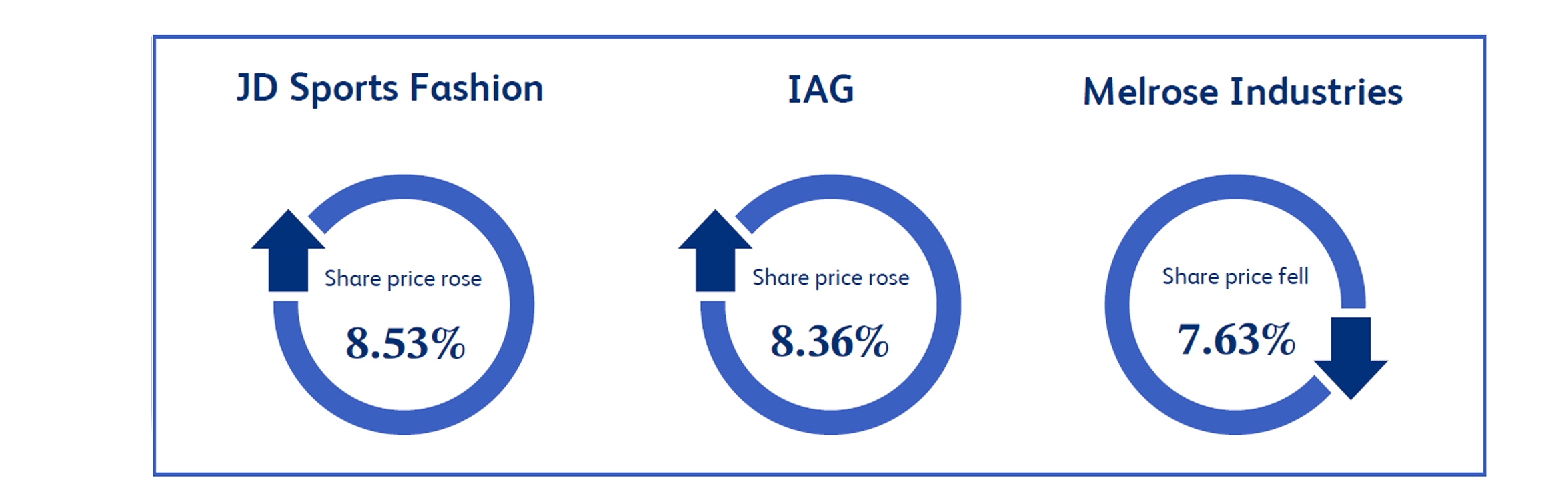

JD Sports Fashion, a high street sports fashion retailer specialising in branded trainers and sportswear, was one of the FTSE’s top performers, after seeing its share price rising 8.53% this week despite the company issuing a cautious outlook and a lower profit forecast. Management warned that sales were impacted by slower product cycles from major footwear partners, and that Middle East tensions could raise supply chain costs. Furthermore, first-quarter sales fell by 2.3%. However, investors responded well to the update, indicating that the market had already anticipated much of the negative news. Sentiment turned positive as some analysts noted that a profit recovery could be on the horizon once underlying margins stabilise, leading buyers to lift the stock.

International Consolidated Airlines Group ("IAG"), a global airline holding company that operates British Airways and Iberia, saw its shares gain 8.36% this week following the successful completion of a €1 billion bond offering. IAG confirmed the full settlement of the senior unsecured bonds, which have now commenced trading on the Irish Stock Exchange. Investors reacted favourably to the news, viewing the successful capital raise as a sign of strong institutional backing and financial stability. The smooth execution of the debt offering reassured the market regarding the group's long-term funding and liquidity position, supporting steady buying pressure throughout the week.

Melrose Industries, an industrial manufacturing group specialising in aerospace and engineering components, was one of the worst performers this week with its shares declining 7.63% after the company reported a chemical storage incident at one of its facilities. The issue involved a tank containing chemicals used in aerospace materials, which triggered temporary local evacuations. Although local officials confirmed that no injuries or leaks occurred and positive progress was made to stabilise the site, the disruption seems to have scared investors. Market sentiment turned cautious as the company began working with customers on operational recovery and supply plans, with shareholders selling down the stock due to concerns over near-term manufacturing delays.

Market Commentary prepared by Walker Crips Investment Management Limited.

This publication is intended to be Walker Crips Investment Management's own commentary on markets. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice you should contact your financial adviser or your usual contact at Walker Crips. Walker Crips Investment Management Limited is authorised and regulated by the Financial Conduct Authority (FRN:226344) and is a member of the London Stock Exchange. Registered office: 128 Queen Victoria Street, London, EC4V 4BJ. Registered in England and Wales number 4774117.

Important Note

No news or research content is a recommendation to deal. It is important to remember that the value of investments and the income from them can go down as well as up, so you could get back less than you invest. If you have any doubts about the suitability of any investment for your circumstances, you should contact your financial advisor.

The value of investments can fall as well as rise. Investors may get back less than invested. Past performance is not a reliable indicator of future results.

The value of investments can fall as well as rise. Investors may get back less than invested.