26 March 2026

This article is the fourth and final in a short series from James Richards, Investment Director at Walker Crips Investment Management, sharing his investment philosophy and the principles that underpin how he manages client portfolios. In these pieces, James explores some commonly held beliefs about investing and explains why long-term outcomes often depend less on fashionable ideas and more on disciplined investment thinking and practical financial planning.

In our recent "Investment Insights" series, we have explored our investment philosophy and why we believe our primary focus of ‘Protect and Compound', is an appropriate ‘all weather’ approach for private client portfolios. As we conclude this series, it is worth reviewing what we mean by ‘protect’ and how we see risk as we try to navigate bull markets as well as surviving the inevitable storms.

Protect and Compound

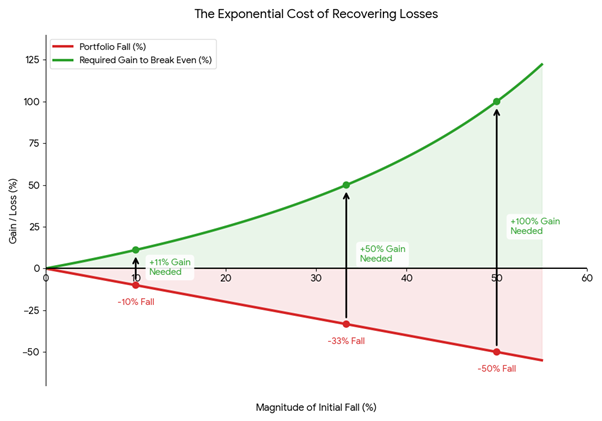

Risk, to us, is the risk of permanent loss of capital. If an investment falls by 10% it needs to return 11% just to get back to the original value. Similarly, if the fall becomes 25%, it must gain 33% before it moves into the black. As such, we care significantly about (and try to avoid) falls in value as participating in large falls probits the compounding effect we look for, whereas if an investment can fall less than the market, it needs to do less work on the upside to compound and outperform over the long term. This capital protection aim is a key financial concept with many investors being specifically ‘loss averse’ rather than ‘risk adverse’. We hope that our Eight Principles and quality focus in our research due diligence will find fund managers and investments that align with this view so that we can make appropriate risk-adjusted returns.

Source: Walker Crips

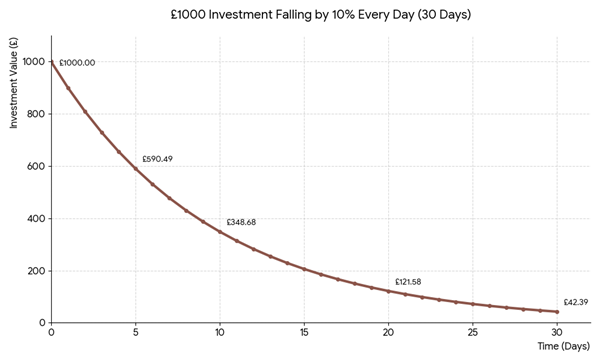

People often use risk interchangeably with volatility, but that isn’t strictly right. Volatility is a measure of the magnitude and direction of change from an average, so (positive) volatility can be a good thing (outperformance). Equally, zero volatility does not mean zero risk - if an investment loses 10% per day every day, it will have zero volatility, but £1,000 would become £42 in a month, a 96% fall in value! That would then need a 2,259% gain just to get back to the starting value of £1,000 - a low volatility but high risk investment!

Source: Walker Crips

Looking at a company’s balance sheet and income statement will give an indication of its financial health: Is it heavily indebted or making profits, has it got good margins or can it service its debt? There are, however, qualitative measures that these statements won't show so analysts do wider research such as speaking to management and staff about culture and the future plans of the business. These can all help inform insights. The better one knows a company and its long-term aims, the better they'll be able to assess whether a negative trading update that causes a share price drop is a short-term blip or a permanent issue. If the former, the negative volatility can actually create a buying opportunity for long-term investors. In contrast, an unjustified positive volatility bout may be a signal to ‘take profits’ and sell. As such, it is important to distinguish between risk and volatility, and to remember that volatility isn’t necessarily a bad thing.

Risk Premium

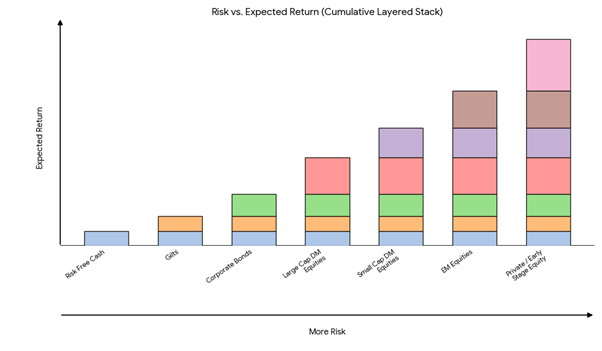

If companies are highly levered or have paper-thin profit margins, they can do well when the sun shines, but will be ‘caught short’ in the bad times, and in extreme cases may go into administration. This can be thought of as higher risk, which investors expect a higher return from as compensation for taking a chance on the firm. This is known as ‘risk premium’, in which there are many different types between asset classes. The chart below shows an indicative view of this where more risk (of loss of capital) should lead, in the long run, to a greater return on investment.

Source: Walker Crips, colours and relative sizes should not be seen as an indication of relative risk premium. The chart is purely indicative.

A balanced portfolio may have a combination of different types of risk assets depending on a number of factors such as the time horizon, return objectives and a client’s willingness to take risk with their investments. Of course, with higher potential highs comes the potential for lower lows and so one should always do bottom-up, fundamental analysis in addition to top-down macroeconomic asset assessments before investing.

Conclusion

Both the tortoise and the hare can be affected by a storm. In a downpour, they will both be swept away, but only the tortoise will be protected by its shell and able to swim once the rains subside, returning to safer ground and carry on chugging along when the sun eventually returns. Both animals can have similar volatility for periods, but carry different underlying risks.

This is why we tend to like those businesses that are not always “sexy”, headline-grabbing firms, instead the seemingly boring but mission-critical firms that remain relevant and resilient throughout an economic cycle and can reinvest to grow the business further.

James Richards, Chartered FCSI

Investment Director

Glossary of Terms

Dividend yield: A financial ratio that shows how much a company pays out in dividends each year relative to its stock price. It is expressed as a percentage.

Gilt: A bond issued by the UK government. They are generally considered lower-risk investments because they are backed by the government.

Total return: The overall return on an investment, combining both capital appreciation (the increase in share price) and any dividends or interest received.

Important information

This article is intended to be Walker Crips Investment Management's own commentary on markets. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice you should contact your financial adviser or your usual contact at Walker Crips. Walker Crips Investment Management Limited is authorised and regulated by the Financial Conduct Authority (FRN:226344) and is a member of the London Stock Exchange. Registered office: 128 Queen Victoria Street, London, EC4V 4BJ. Registered in England and Wales number 4774117.

Important Note

No news or research content is a recommendation to deal. It is important to remember that the value of investments and the income from them can go down as well as up, so you could get back less than you invest. If you have any doubts about the suitability of any investment for your circumstances, you should contact your financial advisor.

The value of investments can fall as well as rise. Investors may get back less than invested. Past performance is not a reliable indicator of future results.

The value of investments can fall as well as rise. Investors may get back less than invested.