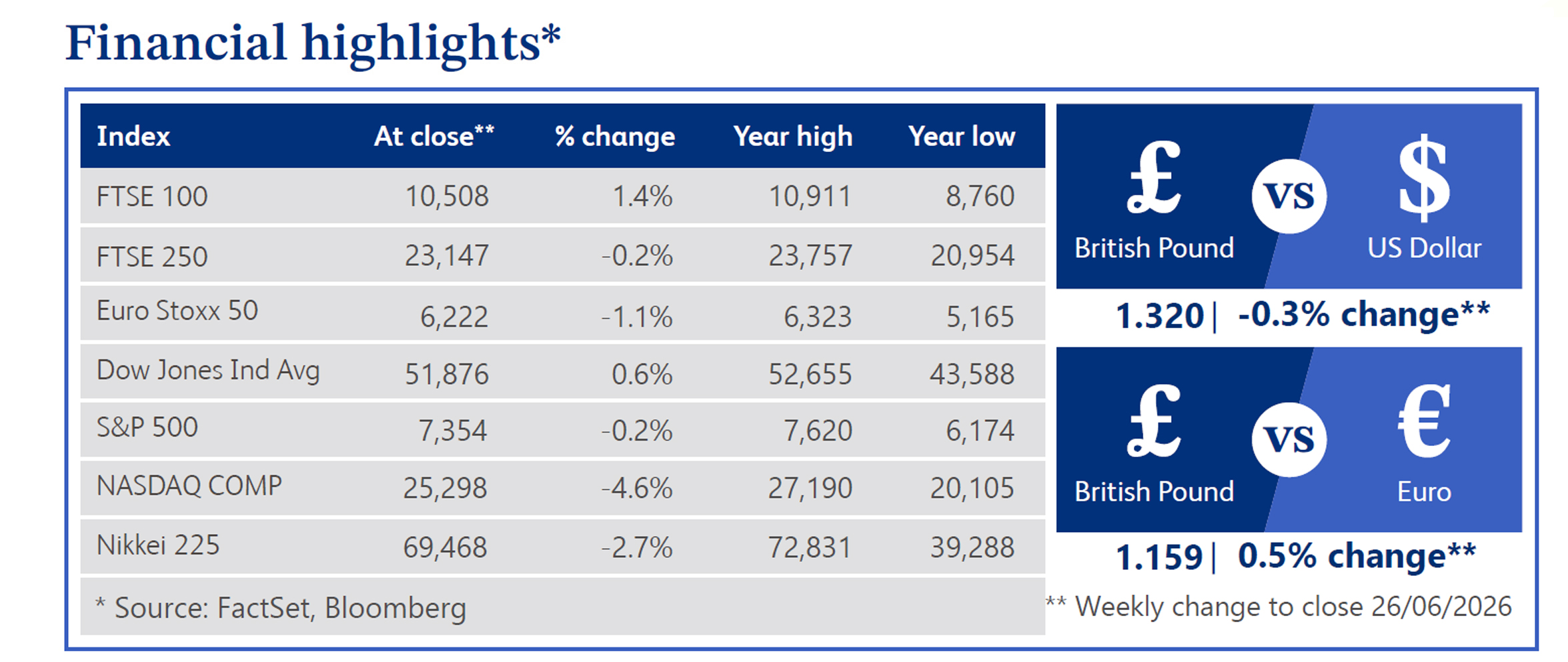

30 June 2026

Last week was marked by the Prime Minister Sir Keir Starmer’s resignation on Monday, despite the exit being expected, anxieties still developed and the British economy continued to stall under cost pressures. The initial hit to corporate confidence was laid bare by a sharp contraction in the flash June Purchasing Managers' Index, as it slumped to a 14-month low. Manufacturing orders hit a six-year low, signalling an immediate freeze in business investment during the leadership transition, whilst Monday morning’s weak Confederation of British Industry Growth Indicator further validated this downwards trajectory. Even though some research data offered a silver lining with public inflation expectations cooling down to 3.8% from 4.7%, the Bank of England remains reluctant to cut interest rates as policymakers are keeping a cautious stance, particularly due to a recent data collection error at the Office for National Statistics which clouded their visibility on the true state of the jobs market.

Sir Keir Starmer’s resignation left a vacuum for possible leaders, leaving the market and Westminster to speculate Andy Burnham’s coronation as all but confirmed. Subsequently, markets are poised for Westminster’s economic blueprint to be reshaped. Burnham promised this Monday a decade-long decentralisation plan covering utilities and infrastructure, while pledging to strictly respect current market-reassuring fiscal rules. Shifting discussions within the cabinet regarding leadership at the Treasury are being closely monitored, with speculation mounting that current Chancellor of the Exchequer, Rachel Reeves, could be demoted in favour of more radical or interventionist figures. Economists within Burnham's inner circle have floated disruptive institutional reforms, from breaking up the Treasury to completely revising the central bank's mandate.

In the markets, traders are demanding fiscal clarity, as the proposed new Prime Minister’s advisers advocate for borrowing billions to fund infrastructure projects. The gilt market remains sensitive to any loosening of fiscal rules, keeping government bonds on edge. However, the utility sector is also under heightened political and regulatory scrutiny as consumer energy debt hit a record high just as bills are set to jump by 13%, and to add further uncertainty for investors, new policy proposals are suggesting the incoming government could step in to nationalise failing energy suppliers. In wider equity markets, sentiment turned defensive as a global tech sell-off bruised London shares.

Across the pond, US equities delivered a mixed performance last week, due to a sharp sector rotation. The equal-weight S&P 500 index outperformed whilst the tech-heavy Nasdaq lagged, dragged lower by Big Tech and semiconductors as investors increased their exposure to cyclicals, healthcare and utilities. Treasuries firmed with a flattening yield curve, while gold declined. Oil retreated to pre-conflict levels last week. However, weekend developments completely upended this optimism with Crude now facing renewed upward pressure following fresh US military strikes, with warnings that Strait of Hormuz shipping will remain restricted. The macro focus pivoted back to the Federal Reserve following resilient economic data with interest rates likely to be hiked by the end of the year.

Segro, a leading European logistics and data centre investor, surged 18.98% last week, as a dramatic rally was triggered after Prologis launched a hostile £12.6 billion all-share takeover bid. Even though the Segro board unanimously and unequivocally rejected the "opportunistic" proposal, arguing it significantly undervalues its growth prospects, the direct appeal to shareholders injected strong momentum into the stock. Whilst shares closed below the implied offer price, the approach sparked a wider rally across British property stocks on hopes of further transatlantic takeovers.

3i Group, an international private equity and infrastructure investor, outperformed by 14.99% last week. This was backed by an upbeat trading statement delivered ahead of its annual general meeting. Management reassured investors that its largest portfolio company, Action, remains firmly on track for strong quarterly profit growth. Even though they are seeing a slight moderation in like-for-like sales growth, the update successfully revived investor confidence in the portfolio's underlying momentum, helping the stock rebound sharply from recent multi-month lows.

Glencore, a globally diversified natural resources company, declined by 7.59% last week, as a tech-led sell-off in Asia continued in Europe. Investor sentiment was severely dented by macroeconomic anxieties, with traders pricing in US interest rate hikes by year-end. This hawkish central bank outlook pushed the US dollar higher, depressing dollar-priced commodities such as copper. In the markets, this macroeconomic pressure completely overshadowed a positive quarterly update that highlighted a 19% increase in own-sourced copper production.

Market Commentary prepared by Walker Crips Investment Management Limited.

This publication is intended to be Walker Crips Investment Management's own commentary on markets. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice you should contact your financial adviser or your usual contact at Walker Crips. Walker Crips Investment Management Limited is authorised and regulated by the Financial Conduct Authority (FRN:226344) and is a member of the London Stock Exchange. Registered office: 128 Queen Victoria Street, London, EC4V 4BJ. Registered in England and Wales number 4774117.

Important Note

No news or research content is a recommendation to deal. It is important to remember that the value of investments and the income from them can go down as well as up, so you could get back less than you invest. If you have any doubts about the suitability of any investment for your circumstances, you should contact your financial advisor.

The value of investments can fall as well as rise. Investors may get back less than invested. Past performance is not a reliable indicator of future results.

The value of investments can fall as well as rise. Investors may get back less than invested.