17 March 2026

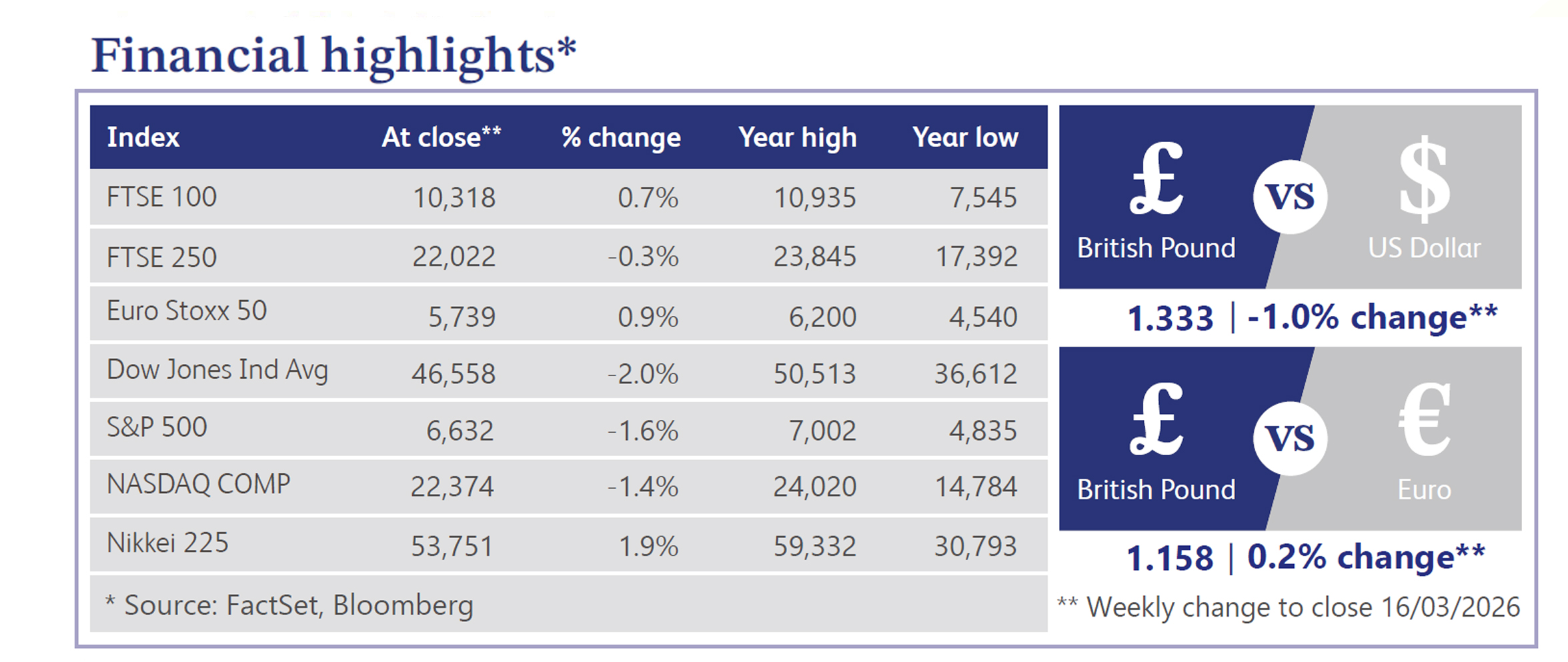

The UK economy was hit by a stagflationary shock this week as Brent crude breached $100 a barrel. Even before the Strait of Hormuz crisis, official data showed Gross Domestic Product (“GDP”) flatlined in January, missing the 0.2% growth forecast, leaving the country vulnerable to the energy supply squeeze. The Office for Budget Responsibility (“OBR”) warned the conflict could drive inflation up to 5% by year-end, wiping out recent progress. Consequently, the Bank of England (“BoE”) is effectively cornered as Money markets are now expecting a 70% chance of a 0.25% hike to 4% by late 2026, abandoning near-term cut hopes. With manufacturing orders collapsing under soaring costs, and households delaying purchases due to inflation fears, the Monetary Policy Committee (“MPC”) must now weigh the risk of cementing a recession against a spiralling, supply-driven price shock.

Labour’s fiscal agenda has been hijacked by this energy vulnerability with the UK now paying Europe's highest gas prices and its supplies fell to two days due to the crisis in the Strait of Hormuz. In response, Prime Minister Kier Starmer coordinated with the US and deployed HMS Dragon to Cyprus to contain the fallout and avoid a wider war. However, this forced the Treasury into crisis management, with Chancellor Rachel Reeves reconsidering fuel duty hikes and the PM announcing an emergency £53 million package for rural households. Such firefighting contrasts with the government’s long-term ambitions of achieving a budget surplus. Westminster remains consumed by the immediate cost-of-living threat.

The financial markets also bore the brunt of this week’s pivot, triggering a violent repricing across UK asset classes. Gilt yields surged, with the two-year yield climbing to its highest since April 2025 as the market reassessed inflation risk and borrowing sustainability during the energy crisis. Equity benchmarks were also set for a weekly loss as $100 oil prices led major banks to delay expected rate cuts, impacting investor sentiment. Yet, despite macro turmoil, cross-border dealmaking showed resilience as a long ownership saga ended, with German Publisher, Axel Springer agreeing to acquire the Telegraph Media Group for £575 million, signalling that premium British assets can still attract foreign capital. Separately, Tesla Energy Ventures received an Ofgem licence to supply electricity, expanding its footprint within domestic and commercial markets.

Across the Atlantic, US equities fell for a third consecutive week as hotter inflation data drove a hawkish recalibration of Federal Reserve (‘Fed”) expectations. Sentiment was weighed down by liquidity concerns in private credit following record redemptions prompted major funds to restrict withdrawals. Treasuries were sold off, while the US Dollar strengthened as gold and silver prices retreated. The Iran conflict remained central as WTI crude surged. While the Trump administration proposed a maritime escort coalition, European and NATO allies, whilst agreeing in the coalition, withheld direct military support, prioritising regional de-escalation despite warnings regarding the alliance's future. Corporate focus shifted to Nvidia’s GTC keynote and UniCredit’s Commerzbank bid, while Meta and Adobe faced volatility amid shifting AI narratives and management departures.

The UK housing market is currently experiencing tension between robust asking prices and declining sentiment. Rightmove noted seasonal growth, but the Royal Institution of Chartered Surveyors (“RICS”) found enquiries falling for the eighth month. Lenders are raising mortgage rates due to energy volatility and inflation.

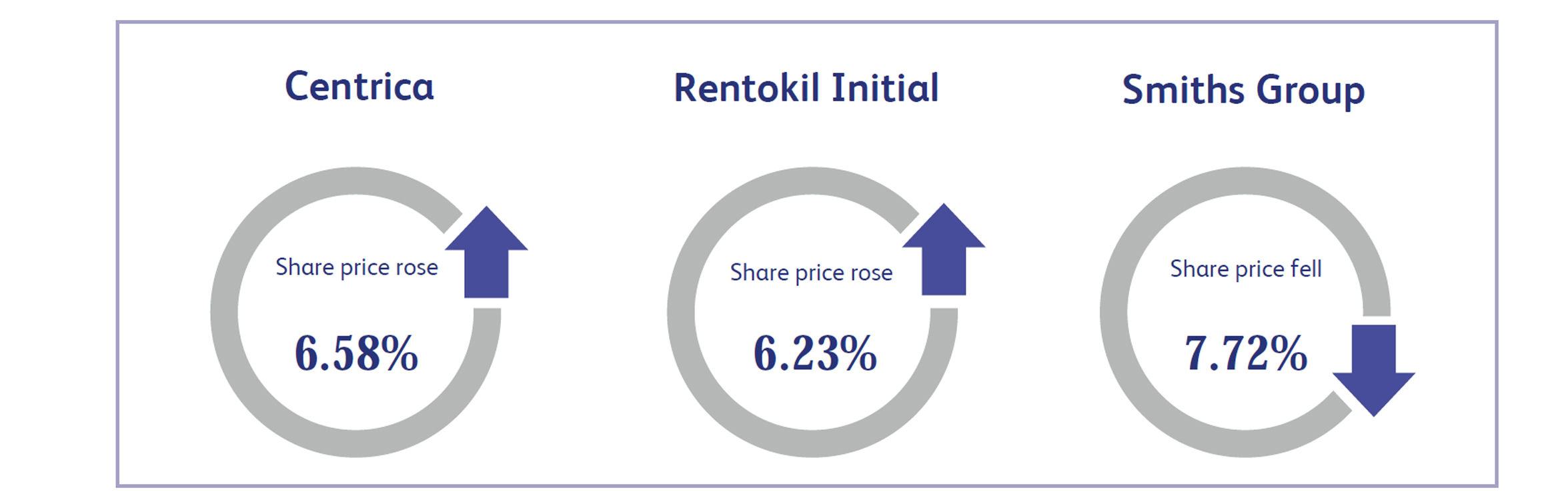

Centrica, a major UK energy supplier and owner of British Gas specialising in gas storage and low-carbon power, advanced 6.58% following optimistic analyst revisions. The company was upgraded as analysts argued that rising geopolitical tensions and volatile gas prices have made its strategic assets increasingly valuable. Sentiment was further bolstered by Centrica’s involvement in a coordinated bid to develop Britain’s first regional hydrogen network in the Humber. While some remain neutral due to a lack of near-term catalysts, the prevailing market mood has improved as many believe the firm is well-positioned to support government objectives around energy security and domestic power generation.

Rentokil Initial, a global leader in pest control and hygiene services with a significant operational footprint in North America, saw its stock rise 6.23%. Despite legacy issues regarding termite claims, the company reported resilient organic growth, indicating that it is successfully navigating its North American recovery and narrowing the valuation gap with its peers. This turnaround stems from a strategic overhaul that pivoted the business towards branch openings to stabilise lead generation and customer retention. Consequently, investor sentiment has brightened significantly, as analysts now expect these operational shifts to improve organic volumes and accelerate earnings over the next year, providing a renewed vote of confidence in the company's trajectory.

Smiths Group, a diversified engineering and technology firm providing specialised components and services to industrial, security, and energy markets, fell 7.72% as debate intensified over its execution story. Market sentiment soured as the stock faced pressure from analysts moving to more cautious ratings, citing growth estimates that sit below the broader market consensus. While some remain positive on the company's long-term plan, the mood amongst investors has become increasingly wary regarding how quickly the firm can deliver on its growth promises at current trading levels. A recent shift in long-term revenue assumptions and split opinions on the execution of its strategy have left the market divided on the company's valuation.

Market Commentary prepared by Walker Crips Investment Management Limited.

This publication is intended to be Walker Crips Investment Management's own commentary on markets. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice you should contact your financial adviser or your usual contact at Walker Crips. Walker Crips Investment Management Limited is authorised and regulated by the Financial Conduct Authority (FRN:226344) and is a member of the London Stock Exchange. Registered office: 128 Queen Victoria Street, London, EC4V 4BJ. Registered in England and Wales number 4774117.

Important Note

No news or research content is a recommendation to deal. It is important to remember that the value of investments and the income from them can go down as well as up, so you could get back less than you invest. If you have any doubts about the suitability of any investment for your circumstances, you should contact your financial advisor.

The value of investments can fall as well as rise. Investors may get back less than invested. Past performance is not a reliable indicator of future results.

The value of investments can fall as well as rise. Investors may get back less than invested.